Blog

“Important Tax Concepts for Retirement”

Tax planning strategies are an essential component to maximizing retirement income. The more income you have in retirement, the more you get to spend or pass down to your heirs. While you might not be making a normal income from employment, considering how taxes will eat into your cashflow is important to think about before you arrive at retirement. Additionally, as tax laws and amounts tend to change depending on the administration in power and our country’s needs, the specific amounts discussed in this article should be seen for informational purposes only.How Much of My Retirement Income will be Taxable?

Understanding what aspects of your retirement income is taxable is a great place to start. The good news is that it’s mostly up to you! The bad news…well , it’s mostly up to you. You have nearly full control of your income decisions in retirement. The goal is clear: to maximize your income while paying the least amount of tax. The first thing you need to know is how our tax system works.How Taxes are Calculated

Ordinary Income Tax Rates

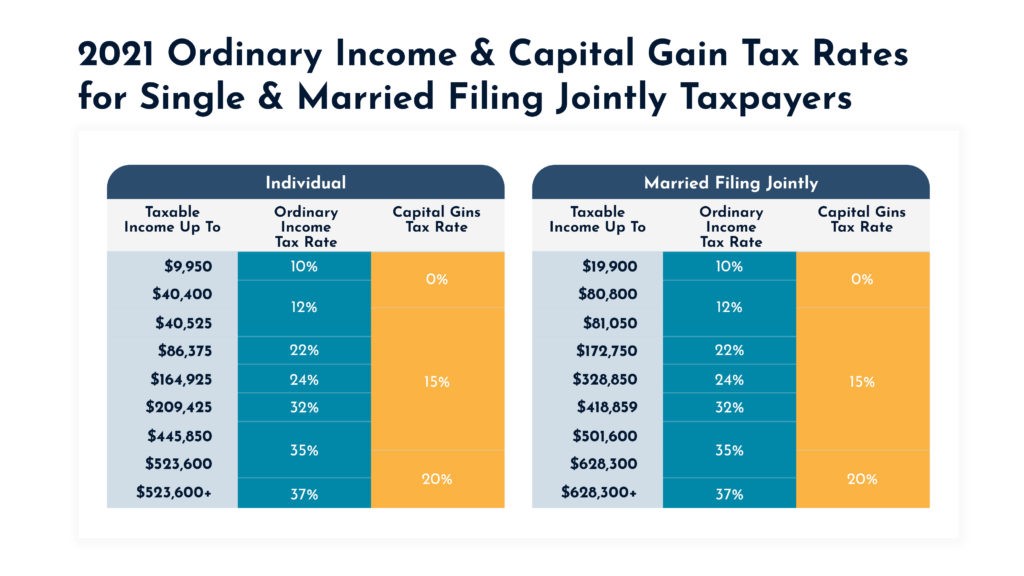

Our federal income tax system is progressive. That means that the percentage of tax increases along with income levels. Ordinary income can consist of wages, salaries, and interest. But more concerning for retirees are taxable Social Security benefits and IRA withdrawals. We all pay federal taxes starting at a rate of 10%. For now, the federal marginal tax brackets go all the way up to 37%. You can see in the chart below what the Individual and Married Filing Jointly tax brackets look like for ordinary income and capital gains in 2021.

Capital Gain Tax Rates

Favorable capital gain tax rates are a key retirement tax planning tool. When you sell a capital asset for more than what you paid for, the result is a capital gain. Capital assets include stocks, bonds, real estate, precious metals, cryptocurrency, etc. If you sell a stock for a profit and hold it for one year it is taxed as a long-term capital gain (LTCG) as shown in the table. You can see that these rates (the far-right column above) are always lower than your marginal tax rates. If you sell a capital asset for a gain that was held for less than a year, the gain is taxed as ordinary income. This is called a short-term capital gain (STCG) and will be subject to your federal marginal tax rates.Withdrawals from Retirement Accounts

Retirement account withdrawals are where you can save BIG on taxes in retirement. This is where all that prudent saving you did in your working years pays off. Without an income distribution plan, you can kiss a lot of those savings’ goodbye to taxes. When thinking about the various accounts you will use for income planning in retirement, it’s important to split them into “taxable accounts “tax deferred accounts”, and “tax free accounts”.Taxable Accounts

Taxable accounts are any non-retirement accounts. Think of your bank or brokerage accounts or that stock certificate your grandparents gave you as a child. For married couples, these accounts are usually jointly owned or in the name of their trust. The capital gain rates that we discussed earlier apply to assets owned in these accounts. In your taxable account is where you need to pay attention to the cost basis and holding periods. Qualified dividends from stocks held in a taxable account are also taxed at lower capital gain rates. But interest income held in a taxable account will be treated as ordinary income, along with STCG’s. As you can see, a sale of an asset here can be subject to two different tax rates. As can the income an asset produces, dividends and interest. And with capital loss rules at your disposal, you can save yourself a lot of money with a good investment strategy. More on that later…Tax-Deferred Accounts

Tax-deferred accounts are the most common types of retirement accounts. Think of 401k’s, 403b’s, IRA’s, and pensions. Every time you contributed to these accounts, that money avoided taxation. There should be a lot of growth from compounding if you have invested it well. Unfortunately, the number you see on your statement that says “Account Value” is not actually all yours. No, you have a silent partner named the IRS that is waiting for your distributions to begin. And when they begin, they will be taxed at ordinary income rates. So, you want to be extra careful when making withdrawals or rollovers from these accounts.Tax-Free Accounts

Roth IRA’s and Roth 401k’s are the only retirement accounts that provide tax-free distributions. Roth accounts are funded with after-tax contributions, so no immediate tax benefit is received. In exchange for foregoing that immediate benefit, all the growth in the account is tax-free, provided certain conditions are met. A Roth is a great account to have in retirement because they allow you to spend more without climbing into a higher marginal bracket. So when you find out you need a new roof, you won’t have an extra tax bill to make things worse. As you think about your income needs in retirement and the corresponding tax brackets it can help to form the most efficient withdrawal strategy. When your nest egg consists of all three types of accounts, you have what we call tax diversification. This diversification makes planning for retirement income much easier and more flexible.Some Final Tax Considerations and Concepts

- Social Security has tax implications – Knowing how much of your social security is taxable is important to understand. Depending on your “combined income”, either 0%, 50%, or 85% of your social security benefits will be subject to taxation.

- Understand and Plan for RMD’s – Required minimum distributions will be required from employer sponsored retirement plans and/or Traditional IRA accounts. From age 72 the IRS will require you to pull a certain amount from these accounts (which will be taxable) each year.

- Asset Location can help determine risk levels – Targeting riskier investments for the accounts with the lowest tax obligations (think stocks in Roth IRA accounts) can be a smart move. If you will pay taxes on income from a Traditional IRA then it can make sense to hold more of your safer performing assets in these accounts which might not see as much growth.

In Summary

Taxes in retirement can seem daunting, but breaking things down into steps can be helpful. The first step is to really think hard about what your retirement will look like. This will give you the answer to a key variable – how much income you need. Next, it’s nice to get familiar with how the U.S. tax code works or ensure you have an expert in your corner who understands this. Taking steps before retirement to ensure tax diversification can help to provide the flexibility to ensure a more fulfilling and rich retirement.Copyright © 2026

Van Gelder Financial